Unlocking Your Financial Potential: Actionable Steps to Boost Your Credit Score

Holding a weak credit score can become a roadblock to fulfilling your financial goals and building a lifestyle you have always dreamed of. A poor credit score can result in limiting your credit access, affecting employment opportunities, and raising borrowing costs. However, do not worry, as you can build a better credit score with the right mindset and strategies. Moreover, with a better credit score, your loan approval becomes quick and easy, and it also welcomes opportunities for low-interest rates on your borrowings.

Importance of a Good Credit Score

Credit score acts as a tool for measuring your debt management ability. As for the lenders, with a high credit score, you are acknowledged as more responsible towards your financial responsibilities. Using the FICO model, a credit score of 850 is considered to be appropriate.

With an acceptable credit score, you can avail easier approval and better loan terms. An excellent or good credit score saves people huge amounts of money throughout their lifetime, as they receive better rates on auto loans, mortgages, and other financial lending.

In addition, individuals scoring a good credit rate are considered lower-risk borrowers, with a higher percentage of banks promoting their businesses by offering better fees, additional perks and rates. On the other hand, individuals with lesser credit scores are considered higher-risk borrowers. Hence, only a few lenders agree on approving their loans, along with a higher interest rate. Not only this, but a poor credit score affects your opportunities to avail rental housing, life insurance policies, and rental cars as your insurance score gets affected by your credit score.

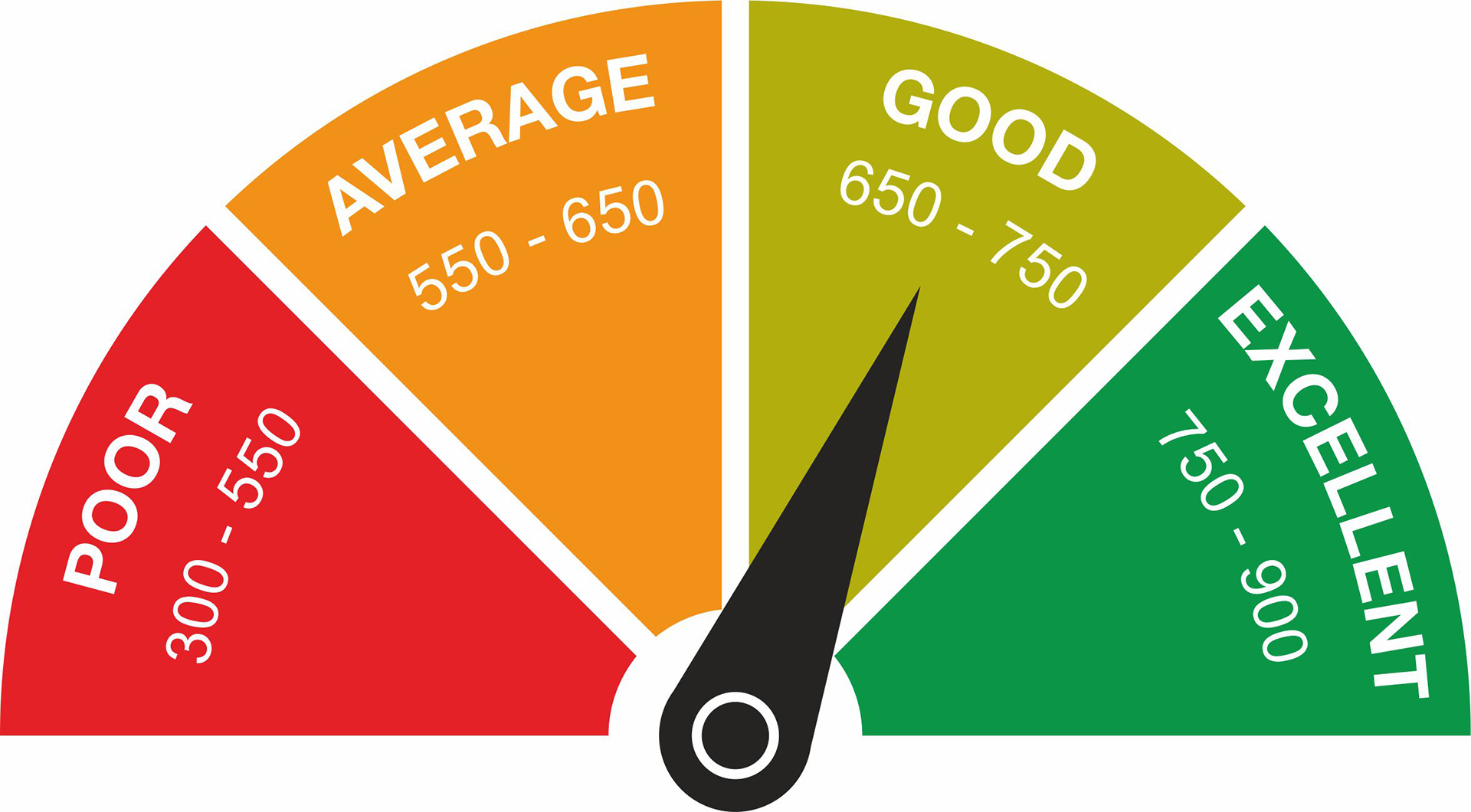

Refer to the table below to understand and check credit score rating:

| Credit Score Range | Rating |

| 300-500 | Poor |

| 550-650 | Average |

| 650-750 | Good |

| 750-900 | Excellent |

Boost your Credit Score

To maintain a good credit score in order to grab better financial opportunities, follow the tips and strategies listed below:

Monitor your Credit Report

Before you begin working on your credit score, you must be aware of your present state. This begins by analysing your credit history. Check credit score using any online financial platforms that are accredited for authenticity. Further, review the report and check the points, increasing or decreasing your score.

Factors positively impacting your credit score include transactions of timely payment, low balance on your credit cards, loan accounts, fewer inquiries for new credit, older credit accounts, and multiple credit cards. Conversely, high credit card balances, judgments, collections, or late or missed payments result in degrading your credit score.

Manage Bill Payments

Over 90% of lenders check credit score to make wise credit decisions. The five factors that determine your score include:

- Credit usage

- Payment history

- Credit mix

- Age of credit accounts

- New credit inquiries

Payment history contributes largely to your credit rating. This is why it is advised to pay your debts on time and responsibly, as it benefits your credit score.

Hence, timely bill payment is the most simple and helpful way of raising your credit score.

Achieve 30% Credit Utilisation or Less

Credit utilisation is that portion of your credit limit that can be utilised at any time. Credit utilisation is the second most important factor, after payment history and score calculation.

To maintain your credit utilisation, try paying off your credit balances each month. However, if not possible, ensure to keep back 30% as your total outstanding balance or even less of the total credit limit. With passing time, you can bring the percentage lower to 10%, which is helpful to raise your credit score.

Another way of raising your credit utilisation ratio is by asking for an increased credit limit. With a higher credit limit, you can manage credit utilisation efficiently.

Consolidate Debt

A number of tools are available that help consumers monitor and manage their credit. Consolidating debt into a good amount and paying off high-interest loans and credit through consolidation is a beneficial step toward increasing your credit score. Consumers must ensure that their credit usage ratio is lower than that of their available line to ensure better credit building.

Limit on New Accounts

Although opening accounts are necessary to build your credit history, you should avoid applying for credit too frequently. Every application may result in a hard inquiry, which may lower your credit score. However, there’s a chance that inquiries will build up and negatively impact your credit scores. Additionally, opening a new account will lower your average account age, which will lower your scores.

Inquiries and your account’s median age are minor score variables. Still, you need to be cautious when it comes to the number of applications you submit. The only exception is if you’re rate shopping for a specific kind of loan, like a home loan or vehicle loan. Since rate shopping is viewed as a low-risk activity, it is possible to overlook some questions if they are raised within a period of a few weeks.

Conclusion

If you are a shopping enthusiast and a frequent user of credit cards, strengthening your credit score is a good step to begin with. It also helps if you’re planning for a new loan application for some major purchases, such as a new home or car, or if you are willing to qualify for the best rewards cards available. You might require a period of weeks to months to notice positive results on your score when following the tips for credit score improvement. By having a regular habit to check credit score, you can look for areas of improvement and build up a good score easily.

FAQs about Check Credit Score

Q1. What are the essential details required to check credit score?

You can check your credit score free of cost by providing certain basic details, including email address, date of birth, mobile number, your name and PAN card.

Q2. How can my credit score help to save money?

You can benefit from lower fees and interest rates for new lines of credit and loans with an excellent credit score.

Q3. Can my credit score change regularly?

Yes, your credit score might fluctuate on a regular basis and even more than once in a single day.

Q4. What is the percentage of payment history in credit score?

Your payment history represents 35% of your credit score. This represents your timely payment, missed payment, and how late you pay your bills.

Q5. Why is there no update on my credit score?

In case you have recently made changes like closing or opening a line of credit or paying your credit card balance, this information might not have been reported to the credit bureaus by your lender yet.

Q6. What are the two major factors in credit score?

Your credit account management and payment history are the two important factors affecting your credit score.